Inflation crises have a way of etching themselves into a nation’s collective memory, leaving scars that shape economic policies for generations. Let’s explore five such crises that not only reshaped national economies but also left an indelible mark on global financial systems.

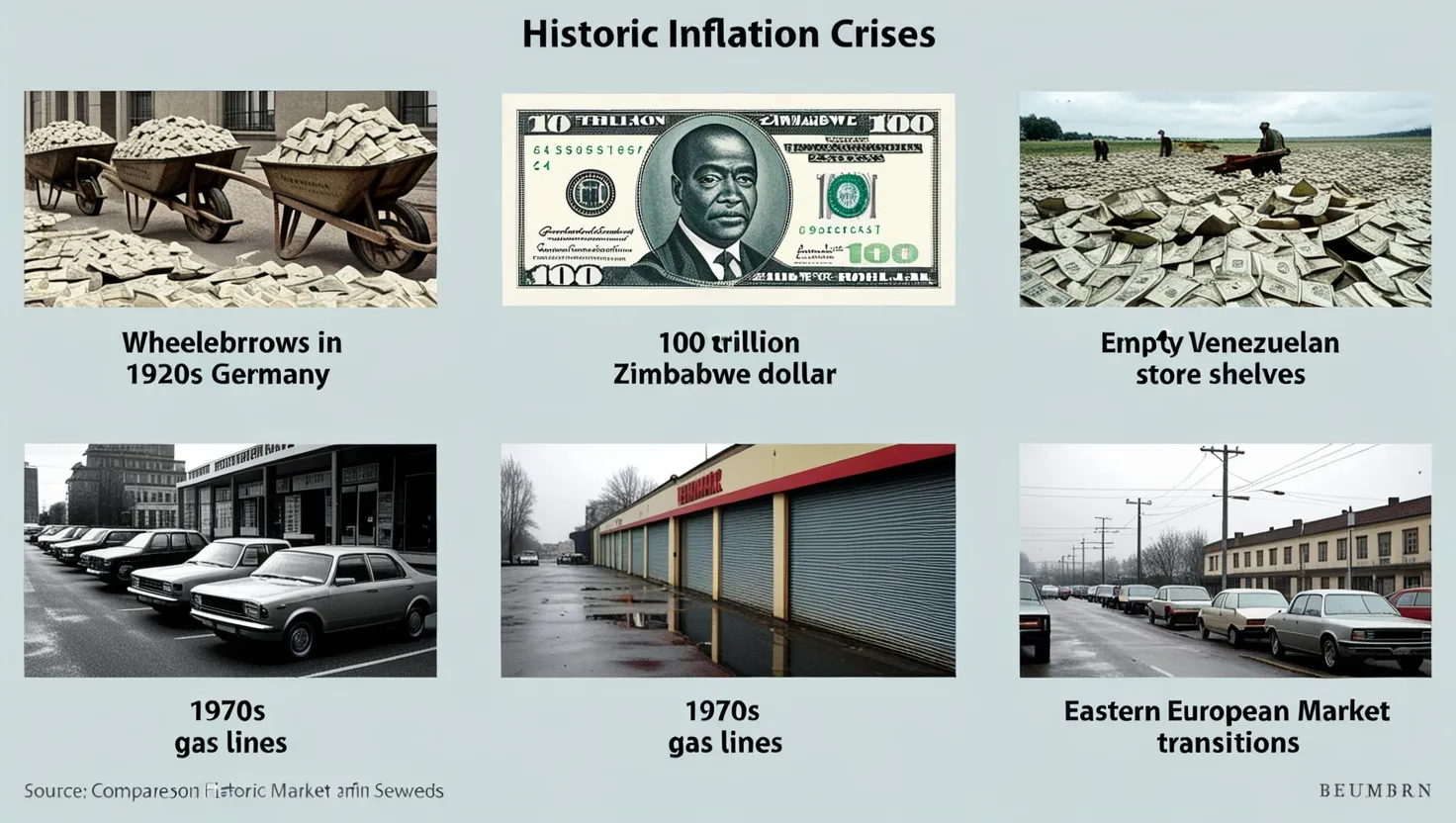

The Weimar Republic’s hyperinflation of 1921-1923 stands as a stark reminder of how quickly a currency can lose its value. Picture this: a loaf of bread that cost 160 marks in 1922 soared to 200 billion marks by late 1923. Can you imagine carrying wheelbarrows of cash just to buy groceries? This wasn’t just an economic crisis; it was a social catastrophe that eroded the very fabric of German society.

“Paper money eventually returns to its intrinsic value – zero.” - Voltaire

The hyperinflation wasn’t merely about numbers; it was about people’s lives unraveling. Savings evaporated overnight, pensions became worthless, and the middle class was effectively wiped out. This economic turmoil created a fertile ground for extremist ideologies. Have you ever wondered how different history might have been if the Weimar Republic had managed to control its inflation?

Fast forward to 2008, and we find ourselves in Zimbabwe, where inflation reached a mind-boggling peak of 79.6 billion percent. Let that sink in for a moment. Prices were doubling every few hours. The government’s response? Printing larger denominations of currency, including a 100 trillion dollar note. It’s almost comical, isn’t it? Except it wasn’t funny for Zimbabweans who saw their livelihoods disappear.

The Zimbabwe crisis teaches us a crucial lesson about the dangers of monetizing government debt and the importance of central bank independence. When a central bank becomes a puppet of the government, printing money to finance deficits, hyperinflation is often the result.

Venezuela’s economic collapse from 2016 to 2019 presents a more recent case of hyperinflation. With inflation rates soaring into the millions of percent, Venezuela’s economy contracted by over 50%. The human cost was staggering – widespread hunger, medicine shortages, and a mass exodus of citizens seeking better lives elsewhere.

“Inflation is taxation without legislation.” - Milton Friedman

What makes Venezuela’s case particularly intriguing is that it occurred in a country with vast oil reserves. It serves as a cautionary tale about the perils of resource dependence and economic mismanagement. How can a country so rich in natural resources fall so far? It’s a question that economists and policymakers continue to grapple with.

The 1970s stagflation in developed economies offers a different flavor of inflation crisis. Unlike the hyperinflation scenarios, this was a period of high inflation combined with economic stagnation and high unemployment. It challenged the prevailing Keynesian economic theories and led to a fundamental rethinking of monetary policy.

The oil shocks of 1973 and 1979 played a significant role in this crisis. As oil prices quadrupled, inflation in the U.S. reached double digits. The Federal Reserve, under Paul Volcker, responded with drastic interest rate hikes, pushing the federal funds rate to a peak of 20% in June 1981. It was a bitter pill to swallow, but it eventually tamed inflation.

This period reshaped central banking globally. It highlighted the importance of inflation targeting and cemented the idea that central banks should prioritize price stability, even at the cost of short-term economic pain. Do you think today’s central bankers are prepared to make similarly tough decisions if faced with runaway inflation?

Lastly, let’s consider the post-Soviet inflation crisis across Eastern Europe from 1991 to 1993. As centrally planned economies transitioned to market-based systems, many experienced severe inflation. In Russia, inflation reached 2,500% in 1992. Poland saw rates of 600%. These countries were essentially building market economies from scratch, and the process was painful.

“Inflation is as violent as a mugger, as frightening as an armed robber and as deadly as a hit man.” - Ronald Reagan

This crisis underscored the challenges of economic transition and the importance of institutional frameworks in managing inflation. It led to the adoption of currency board arrangements in some countries and accelerated the push for European Union membership as a means of achieving economic stability.

Each of these crises left lasting legacies. They shaped modern inflation targeting frameworks, influenced currency management practices, and underscored the importance of central bank independence. Today’s central bankers design policies with these historical lessons in mind, aiming to avoid the devastating economic episodes that destabilized societies and undermined public trust in financial institutions.

But as we reflect on these crises, we must ask ourselves: Are we truly safe from such events in the future? Have we learned enough from history to prevent similar catastrophes? Or are we simply setting ourselves up for new forms of economic instability?

The truth is, while we’ve made significant strides in understanding and managing inflation, the global economy is more interconnected and complex than ever before. New challenges, from climate change to technological disruptions, could create inflationary pressures we’re not prepared for.

Moreover, the unprecedented monetary policies adopted in response to the 2008 financial crisis and the COVID-19 pandemic have pushed us into uncharted territory. Central banks have expanded their balance sheets to levels never seen before. While this hasn’t led to high inflation yet, some economists warn that we may be sitting on a ticking time bomb.

As we navigate these uncertain waters, it’s crucial to remember the human cost of inflation crises. Behind every percentage point of inflation are real people struggling to make ends meet, businesses fighting to stay afloat, and dreams being deferred or destroyed.

Perhaps the most important lesson from these crises is the need for vigilance and adaptability. Economic stability should never be taken for granted. It requires constant attention, thoughtful policies, and a willingness to make tough decisions when necessary.

So, as we look to the future, let’s carry these lessons with us. Let’s remember the wheelbarrows of cash in Weimar Germany, the worthless trillion-dollar notes in Zimbabwe, the empty shelves in Venezuela, the stagflation of the 1970s, and the painful transitions in Eastern Europe. These memories should serve not as distant historical curiosities, but as urgent reminders of what’s at stake in the ongoing battle for economic stability.

What role can you play in this? How can we, as citizens, contribute to economic stability? Perhaps it starts with financial literacy, with understanding the forces that shape our economy. Perhaps it involves holding our leaders accountable for their economic decisions. Or maybe it’s about building resilient communities that can weather economic storms.

Whatever the answer, one thing is clear: the fight against destructive inflation is not just a task for economists and policymakers. It’s a collective responsibility, a shared mission to create a more stable and prosperous future for all. Are we up to the challenge?