Money Makeover: Smart Moves for Life's Big Changes

Navigate life's financial shifts with Maya: from marriage to parenthood and career changes. Learn to adapt money strategies for long-term success and stability.

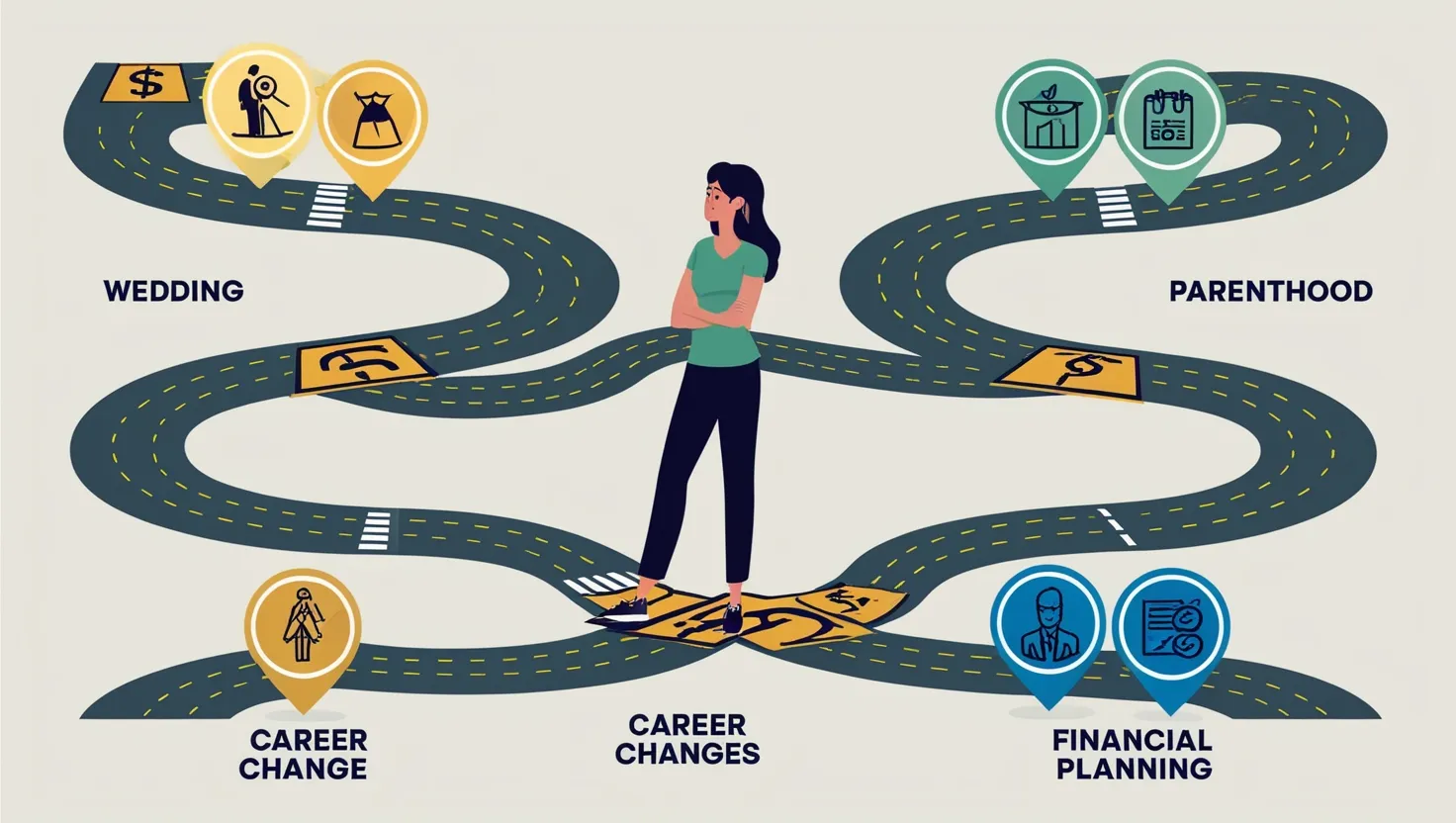

As we navigate the intricate dance of life, major transitions can significantly reshape our financial landscapes, requiring us to adapt and refine our money management strategies. Let’s follow Maya, a young professional, as she embarks on a journey through several life-changing events, each demanding a unique financial rhythm.

Maya’s first significant transition is getting married. What seems like a joyous celebration also becomes a crash course in budgeting and prioritizing expenses. She quickly learns that wedding planning is not just about choosing the perfect venue or dress, but also about managing the financial implications of merging two households. This involves consolidating debts, creating a joint budget, and making decisions about shared financial goals. For instance, Maya and her partner must decide whether to combine their bank accounts, how to split expenses, and how to allocate their savings towards common goals like buying a home or starting a family.

As Maya and her partner prepare for parenthood, they are introduced to the world of long-term financial planning. This phase is not just about saving for diapers and childcare; it’s also about securing their family’s financial future through insurance and investment. Maya discovers the importance of life insurance, health insurance, and even disability insurance to protect their income in case of unexpected events. She also starts exploring options for saving for her child’s education, such as 529 college savings plans, which offer tax benefits and help in building a substantial fund over time.

When Maya decides to start a family, her financial priorities shift dramatically. She must balance the immediate costs of raising a child with long-term financial goals. This includes adjusting her budget to accommodate new expenses like childcare, healthcare, and education. Maya also learns about the value of flexible spending accounts (FSAs) and dependent care FSAs, which can help reduce her taxable income by setting aside pre-tax dollars for childcare expenses.

As her family grows, Maya faces another significant transition: changing careers. This decision is driven by a desire for better work-life balance and greater financial stability. However, it also presents short-term financial constraints, such as a potential reduction in income during the transition period. To navigate this, Maya focuses on cash flow optimization, ensuring she has an emergency fund in place to cover at least six months of living expenses. She also invests in relevant training and networking opportunities to enhance her career prospects and earning potential.

Changing careers also prompts Maya to rebalance her investments. She realizes that her investment strategy needs to align with her new career goals and risk tolerance. This involves reassessing her asset allocation, considering whether to shift from high-risk investments to more stable ones, and exploring tax-advantaged retirement accounts like 401(k) or IRA. Maya understands that investing in her future is a long-term game and that each career transition offers an opportunity to refine her investment strategy.

Throughout these transitions, Maya learns the importance of risk management. She understands that life is full of uncertainties and that having a robust risk management plan can protect her family’s financial well-being. This includes diversifying her investments, maintaining adequate insurance coverage, and building an emergency fund. Maya also explores alternative income streams, such as part-time work, freelancing, or even starting a small business, to ensure she has multiple sources of income.

Divorce or separation, though not part of Maya’s journey, is another significant life transition that can have profound financial implications. For those facing this challenge, it’s crucial to reevaluate financial goals and establish financial independence. This involves dividing assets, adjusting income and expenses, and dealing with legal costs. It’s also important to consider the impact on retirement earnings and assets, as well as the effects on employment and retirement decisions post-divorce.

In addition to these personal transitions, external factors like career changes, health challenges, or financial shifts can also impact one’s financial landscape. For instance, a job change may involve comparing total compensation packages, including salary, benefits, and retirement savings. It may also require rolling over superannuation balances to maintain retirement savings momentum. During periods of unemployment or career transition, crafting a financially resilient strategy is essential, involving budgeting, cutting unnecessary costs, and exploring alternative income streams.

Maya’s journey highlights the importance of financial education and literacy. She invests time in courses on personal finance, joins relevant online communities, and follows reputable financial blogs. This knowledge empowers her to make informed decisions about her money, from managing debt to investing in her future. Maya realizes that financial independence is not just about having wealth; it’s about having the power to produce wealth through her skills, knowledge, and adaptability.

As Maya navigates these life transitions, she discovers that defining or redefining her life purpose is crucial. Knowing her purpose keeps her motivated to improve her financial situation, as it aligns with her values and principles. This purpose-driven approach helps her stay focused on her financial goals, even during times of significant change.

In conclusion, life transitions are inevitable, and each phase brings its own set of financial challenges and opportunities. By staying nimble, adapting financial strategies, and leveraging these transitions as opportunities for growth, individuals like Maya can maintain financial stability and achieve long-term financial success. This dynamic dance of personal finance requires flexibility, rhythm, and occasional improvisation, but with the right mindset and knowledge, anyone can navigate life’s economic shifts successfully.